Authors: Shivani Sharma, Ritika Singh Thakur

Abstract

India’s mandatory Corporate Social Responsibility (CSR) regime under Section 135 of the Companies Act, 2013, institutionalised corporate participation in social and environmental development through the “2% rule”. While biodiversity conservation has been formally recognised under Schedule VII of the said Act, its integration into corporate decision-making has remained limited. This study examines whether India’s CSR regime can meaningfully confront the consistent environmental neglect by embedding biodiversity protection and sustainability within the corporate governance systems. Using a mixed-method approach combining legal analysis, policy review, case studies, and comparative insights from selected European countries (here, the UK, France, and Germany), the study has identified a structural bias toward restoration-based, expenditure-driven interventions rather than long-term biodiversity protection. CSR reporting frameworks, including SEBI’s BRSR disclosures, emphasise financial allocation over ecological outcomes, resulting in symbolic compliance and fragmented conservation efforts. A governance mismatch between CSR law and the Biological Diversity Act, 2002 further weakens accountability and benefit-sharing linkages. The study argues for recalibrating India’s CSR framework through biodiversity risk integration, outcome-based metrics, stronger alignment with biodiversity law, and convergence with global nature-disclosure systems such as TNFD and CSRD. Hence, reimagining CSR beyond the 2% rule requires shifting biodiversity from philanthropic expenditure to justiciable ecological responsibility and strategic risk governance within corporate decision-making.

Keywords

Corporate Social Responsibility (CSR), Biodiversity Governance, Environmental Constitutionalism, Sustainability, Great Indian Bustard, Companies Act 2013, TNFD, CSRD.

Introduction

What had begun as a discretionary charity, guided by the Voluntary Guidelines on Corporate Social Responsibility (CSR) issued in 2009 and later refined in 2011, was institutionalised through Section 135 of the Companies Act, 2013. With this legislative move, India emerged as one of the first countries to legally require qualifying companies to allocate financial resources toward social and environmental development. The evolution of CSR in India from a voluntary philanthropic practice to a mandated legal obligation represents a transformative shift in the engagement between the corporations, the state, and the civil society.

The regulatory framework is principally structured around the widely recognised “2% rule.” Companies that meet prescribed financial thresholds—net worth of ₹500 crore, turnover of ₹1,000 crore, or net profit of ₹5 crore—are obligated to spend at least 2% of their average net profits on CSR activities enumerated under Schedule VII of the Act. While this mandate has mobilised substantial corporate funding for developmental initiatives, its potential to address pressing ecological concerns, especially biodiversity loss and climate vulnerability, has remained underutilised and requires critical re-examination. Ecological restoration has often been preferred over biodiversity conservation.

Biodiversity, as defined by the Convention on Biological Diversity, encompasses the variability of life across terrestrial and aquatic ecosystems, underpinning ecological sustainability; yet India protects under 6% of its land, with continued species decline indicating limited conservation progress. Schedule VII, specifically item (iv), includes provisions for environmental sustainability, ecological balance, and the protection of flora and fauna. However, corporate engagement in this domain has often been limited to short-term, measurable, and visibility-driven interventions, many of which border on reputational exercises rather than substantive ecological investment. Recognising this limitation, the amended CSR Rules introduced the concept of “Ongoing Projects,” enabling companies to undertake multi-year initiatives extending up to three years beyond the year of initiation. This regulatory flexibility creates an enabling pathway for long-term biodiversity conservation and ecological restoration programs that require sustained financing and monitoring.

Against this backdrop, the present research examines how corporations can strategically utilise India’s evolving CSR legal framework—through partnerships with registered implementing agencies, long-term project structuring, and the carry-forward set-off of excess expenditure—to transition from compliance-driven spending to a restorative sustainability model capable of safeguarding India’s biodiversity future.

Theoretical Background

With the enactment of Section 135 of the Companies Act, 2013, CSR became a mandatory obligation requiring eligible companies to allocate at least 2% of their average net profits toward socially and environmentally beneficial activities (Ministry of Corporate Affairs [MCA], 2013). This shift institutionalised CSR within corporate governance structures and relocated environmental accountability from discretionary management practice to board-level responsibility (Chatterjee & Mitra, 2017; MCA Circular No.14/2021). While the mandate formally integrates social investment into corporate decision-making, empirical assessments indicate that corporate participation remains largely compliance-driven, with firms clustering around the statutory minimum rather than embedding sustainability into core strategy (Dharmapala & Khanna, 2018; Bansal et al., 2015).

Scholarly discourse increasingly conceptualises CSR “beyond compliance.” Drawing on stakeholder theory (Freeman, 1984), legitimacy theory (Suchman, 1995), and shared value theory (Porter & Kramer, 2011), it has been argued that CSR must move beyond financial allocation to generate measurable ecological and societal value. Sustainability scholarship further aligns CSR with ESG performance, emphasising risk governance, responsible business conduct, and outcome-based accountability (Eccles & Klimenko, 2019). The “Chatterjee Model” advances this shift by framing CSR as a structured and scientific process aligned with national development goals through “projectivation”—the formalisation of projects with defined budgets, personnel, timelines, and measurable outcomes (Chatterjee & Mitra, 2017; Rathod, 2023). In this sense, CSR operates as regulated self-regulation, compelling firms to internalise environmental considerations within commercial frameworks (Ganesh & Venugopal, 2024; Singh & Sahay, 2025).

Despite this regulatory innovation, structural limitations within the 2% mandate persist. A financial quantification bias wherein CSR performance is assessed primarily through expenditure rather than ecological outcomes has been identified (Garg et al., 2020). Annual reporting cycles generate temporal short-termism, discouraging long-gestation ecological initiatives such as watershed or biodiversity restoration (KPMG, 2022). Corporations often prioritise low-risk, visible and measurable initiatives, such as plantation drives or awareness campaigns, producing what has been described as symbolic environmentalism (Garg et al., 2020; KPMG, 2022). Empirical spending patterns reinforce this critique- education, rural development, and healthcare receive significantly higher allocations than environmental sustainability (Rathod, 2023; Garg et al., 2020). In some instances, major corporations reportedly allocated 0% of their CSR budgets specifically to environmental sustainability during FY2020–21 (Rathod, 2023), reflecting sectoral imbalance and limited prioritisation of biodiversity conservation and protection.

Within this framework, biodiversity conservation has emerged as both a governance and risk issue. Schedule VII of the Companies Act explicitly permits CSR spending on environmental sustainability, conservation of flora and fauna, afforestation, and ecological balance (MCA, 2013; Singh, 2025; Ganesh & Venugopal, 2024). However, biodiversity remains among the least operationalised CSR domains. Institutional constraints—such as the absence of biodiversity accounting frameworks, limited ecological expertise within CSR departments, and weak monitoring systems—have hindered meaningful implementation (UNEP, 2010; IUCN, 2016).

Biodiversity has also been reframed as a material corporate risk. More than half of global GDP depends on nature, and in India, sectors such as agriculture, fisheries, and energy remain highly vulnerable to ecosystem degradation (Slootweg, 2012; Trim, 2025). Businesses confront three tiers of risk: physical risks stemming from ecosystem loss; regulatory and legal risks, including liability and compliance costs; and reputational risks that affect market position (Slootweg, 2012). Effective governance, therefore, requires integrating biodiversity into Enterprise Risk Management by identifying Dependencies, Impacts, Risks, and Opportunities (DIRO) (Trim, 2025).

Sector-specific scholarship has underscored the urgency of such integration in extractive industries. Mining and metals operations cause deforestation, biodiversity loss, land degradation, and hydrological disruption (Hilson, 2012). In aluminium value chains, for instance, environmental impacts include forest diversion, red mud disposal, fly ash contamination, and groundwater depletion (Dashwood, 2012; Hilson, 2012). Yet CSR spending in these sectors often remains welfare-oriented, producing what has been termed externality displacement—where social expenditure does not correspond materially or geographically to ecological harm (Dashwood, 2012). CSR is frequently deployed to secure a social licence to operate rather than to deliver ecological restitution (Gunningham et al., 2004).

Although the Local Area Preference principle seeks to prioritise communities surrounding industrial operations (MCA, 2013), pollution-intensive industrial belts continue to experience environmental degradation and public health vulnerabilities (Hilson, 2012). This produces a geography–accountability gap between sustainability reporting and lived environmental realities (Dashwood, 2012). Legal scholarship further complicates the CSR landscape by examining its interface with enforceable environmental statutes such as the Biological Diversity Act, 2002 (National Biodiversity Authority [NBA], 2002). Judicial expansion of environmental rights jurisprudence has strengthened the concept of justiciable environmental responsibility, challenging the sufficiency of voluntary CSR mechanisms (Kotler & Lee, 2005).

Recent governance reforms indicate movement toward disclosure-based accountability. India’s Business Responsibility and Sustainability Reporting (BRSR) framework and SEBI ESG mandates expand transparency obligations (Securities and Exchange Board of India [SEBI], 2021). However, biodiversity disclosure metrics remain underdeveloped, constraining natural capital assessment (Addison et al., 2019). Internationally, frameworks such as the Taskforce on Nature-related Financial Disclosures (TNFD) and the Corporate Sustainability Reporting Directive (CSRD) institutionalise biodiversity risk disclosure, signalling a shift from expenditure-driven CSR toward risk-based ecological accountability (Addison et al., 2019).

To bridge the materiality gap, structured impact measurement tools have been advocated. The Pressure-State-Response-Benefit (PSRB) framework links environmental pressures, ecological conditions, corporate responses, and socio-ecological benefits (Andreasson, 2023). Tools such as the Integrated Biodiversity Assessment Tool (IBAT) and the Global Biodiversity Score (GBS) enable firms to quantify biodiversity footprints and establish SMART targets, including “No Net Loss” or “Net Positive Impact” commitments (Andreasson, 2023).

Overall, a paradox has emerged on the foreground. India’s CSR regime provides a robust statutory and conceptual foundation for integrating biodiversity into corporate governance. Yet structural biases toward expenditure reporting, sectoral imbalances, weak biodiversity metrics, and limited alignment with global nature-risk disclosure systems constrain ecological outcomes. Emerging scholarship, therefore, calls for an impact-based CSR paradigm—shifting from philanthropic spending to ecological restitution, from compliance to measurable restoration, and from symbolic environmentalism to accountable sustainability governance (Eccles & Klimenko, 2019).

Financial and Strategic Evolution of CSR Beyond the 2% Rule

Table 1: CSR Expenditure, Intensity, and Environmental Allocation Trends (2019–2024)

| Firm | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | CSR Intensity Range | Env CSR Range |

| Tata Steel | 314 | 331 | 387 | 480 | 580 | 2.0–2.4% | 26–29% |

| Vedanta Ltd. | 270 | 301 | 399 | 412 | 450 | 2.0–2.4% | 26–30% |

| Hindalco | 176 | 182 | 210 | 238 | 265 | 2.0–2.3% | 25–27% |

| NMDC | 118 | 132 | 150 | 168 | 195 | 2.0–2.4% | 27–29% |

| Coal India | 421 | 415 | 433 | 462 | 498 | 2.0–2.3% | 23–27% |

| Hindustan Zinc | 82 | 96 | 109 | 124 | 140 | 2.0–2.4% | 32–35% |

The data reveals a consistent upward trajectory in CSR expenditure across all sampled firms, with companies such as Tata Steel and Vedanta Ltd. demonstrating significant scaling of sustainability investments. CSR intensity ratios have gradually moved beyond the statutory 2% threshold, while the environmental CSR share has expanded to nearly 30% in several firms. However, biodiversity-specific spending remains embedded within this broader environmental allocation, indicating a persistent financing gap for ecosystem restoration initiatives.

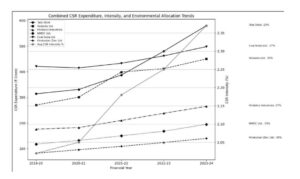

Figure 1: Graphical Representation of CSR Expenditure, Intensity, and Environmental Allocation Trends (2019–2024)

Fig. 1 Illustrates a steady upward trajectory in CSR expenditure across all sampled firms between FY2019–20 and FY2023–24. Companies such as Tata Steel and Vedanta Ltd. demonstrate substantial scaling of CSR budgets, while Coal India Ltd. maintains the highest absolute expenditure levels throughout the period. Smaller firms such as NMDC and Hindustan Zinc show proportionate growth, indicating sector-wide expansion rather than isolated corporate behaviour.

The secondary axis reflects CSR intensity, which shows a gradual increase from approximately 2.05% to nearly 2.35%, suggesting that firms are not merely meeting but modestly exceeding the statutory mandate under the Companies Act 2013. This indicates a shift from minimum compliance toward strategic allocation.

Environmental CSR allocation percentages (annotated alongside the graph) range between 23% and 35%, with Hindustan Zinc exhibiting the highest proportional environmental commitment. However, despite this growth, biodiversity-specific spending remains embedded within broader environmental categories, reinforcing the structural argument that ecological financing expansion has not translated into targeted biodiversity prioritisation.

Overall, the visual trend confirms two simultaneous dynamics: expansion of CSR financial pools and incremental growth in environmental allocations, yet without a proportional reorientation toward biodiversity-centred governance.

Legal and Policy Framework: Conceptualising Environmental Responsibility in India’s Business Framework

India’s approach to environmental responsibility in business is normatively anchored in Principle 6 of the National Guidelines on Responsible Business Conduct (NGRBC), which requires enterprises to “respect and make efforts to protect and restore the environment.” This represents a deliberate policy shift away from narrow regulatory compliance toward a proactive, integrated model of responsible business conduct, aligned with the “triple bottom line” of people, planet, and profit.

Crucially, the policy framework has conceptualised environmental protection not as an external constraint on business, but as a core managerial and governance responsibility embedded across corporate operations and value chains. However, the extent to which this policy vision translates into meaningful corporate action depends heavily on the design and limitations of the underlying legal framework, particularly CSR law and associated disclosure regimes.

Core Pillars of Environmental Responsibility: Policy Commitments

Indian policy instruments articulate environmental responsibility through five interrelated pillars:

- Life-cycle responsibility, requiring businesses to account for environmental impacts across the full product life cycle—from extraction and design to consumption and disposal—rather than limiting responsibility to operational sites.

- The precautionary principle, encouraging avoidance of environmentally harmful actions even under scientific uncertainty, prioritises prevention over remediation.

- Resource efficiency and circularity, emphasising reduced material intensity, reuse, recycling, and circular economy models.

- Pollution prevention and accountability, reflecting a functional application of the “polluter pays” principle through emissions monitoring and cost internalisation.

- Climate mitigation and resilience, extending corporate responsibility to emissions reduction, energy efficiency, and adaptation planning.

These pillars establish a high normative bar for corporate environmental conduct. Biodiversity protection, however, occupies a more ambiguous position within this framework.

Positioning Biodiversity within the Environmental Policy Architecture

Biodiversity is recognised in policy as foundational to ecological stability and sustainable growth, yet it remains weakly operationalised. It enters the framework in four principal ways:

- As a performance indicator, encourage biodiversity-related metrics;

- Through restoration and protection mandates, including ecosystem rehabilitation;

- Via safeguards for ecologically sensitive areas, requiring heightened due diligence;

- Through equitable benefit-sharing, particularly with communities associated with biological resources and traditional knowledge.

Supporting instruments such as the National Forest Policy (1988) reinforce this framing by recognising forests as genetic reservoirs. Nevertheless, biodiversity is largely treated as a subset of environmental sustainability, rather than as a distinct governance priority with specific legal and financial requirements.

From Policy Vision to Practice: Reporting and Disclosure Mechanisms

The transition from the Business Responsibility Report (BRR) to SEBI’s Business Responsibility and Sustainability Report (BRSR) represents an institutional effort to operationalise environmental responsibility through standardised disclosures. The BRSR mandates ESG reporting by the top 1,000 listed companies, including disclosures related to biodiversity impacts and emerging mechanisms such as Green Credits.

However, the regulatory emphasis remains disclosure-oriented rather than outcome-driven. Reporting obligations measure what is reported, not what is restored, limiting the framework’s capacity to drive substantive biodiversity conservation.

Table 2: Quantifying Symbolic vs. Substantive Compliance

| Disclosure Category | Indicators from Sources | Nature of Compliance |

|---|---|---|

| Essential Indicators | Waste management, emissions, and resource usage. | Mandatory & Reporting-oriented: Measures “what is reported, not what is restored”. |

| Leadership Indicators | Specific biodiversity impacts and value-chain disclosures. | Voluntary & Outcome-oriented: Often ignored due to “spending-centric” culture. |

| Geographical Focus | Local industrial/urban locations. | Spatially Biased: Sidelines remote biodiversity hotspots in favour of easy proximity. |

| Administrative Spend | Capped administrative and monitoring costs. | Low Rigour: Limits hiring of scientific expertise for long-term evaluation. |

Corporate Role in Biodiversity Governance: Policy Expectations versus Legal Reality

India’s environmental and biodiversity policies—most notably the National Environment Policy (2006) and the National Biodiversity Action Plan (NBAP)—envision corporations as active partners in conservation, and not merely compliance actors. Corporations are encouraged to contribute through:

- Multi-stakeholder partnerships for afforestation, habitat restoration, and waste management;

- CSR-led community interventions, particularly in environmental education and awareness;

- Innovation and R&D, positioning the private sector as a driver of biodiversity monitoring tools and clean technologies;

- Voluntary standards and market mechanisms, including ISO certifications, ecolabelling, and natural resource accounting.

Despite these expectations, institutional coordination between biodiversity governance and CSR planning remains weak, resulting in project-based, ad hoc engagement rather than systemic integration.

Legal Framework Governing CSR, Environment, and Biodiversity

CSR Law as the Primary Legal Interface

The legal foundation for CSR-driven environmental action is established under Section 135 of the Companies Act, 2013, Schedule VII, the CSR Rules, and ministerial clarifications. These provisions explicitly permit CSR expenditure on:

- Environmental sustainability and ecological balance;

- Conservation of natural resources;

- Agroforestry and animal welfare;

- River rejuvenation and sanitation;

- SDG-aligned research and development.

While biodiversity-related activities are clearly recognised as permissible CSR interventions, the legal framework frames them predominantly as short-term projects, and not as long-term ecological commitments aligned with policy goals.

Ancillary provisions—such as the integrated definition of CSR, local area preference, SDG alignment, impact assessment requirements, and constitutional grounding under Articles 48A and 51A(g)—reinforce the environmental mandate. Yet their design features significantly shape corporate behaviour, often in ways that conflict with biodiversity realities.

Structural Legal Constraints Undermining Policy Objectives

Several features of CSR law help explain the gap between policy ambition and on-ground biodiversity outcomes:

- Short project time horizons, with “ongoing projects” capped at three financial years beyond commencement, are fundamentally misaligned with decadal ecological restoration timelines.

- Annualised, profit-linked spending obligations introduce funding volatility, discouraging long-term biodiversity investments that require stable financing.

- “Use-it-or-lose-it” compliance pressure, backed by stringent penalties, incentivises easily executable projects over complex ecological interventions.

- Local area preference, though, biases CSR spending toward industrial or urban locations, sidelining remote biodiversity hotspots.

- Caps on administrative and monitoring costs limit the feasibility of scientifically rigorous biodiversity projects requiring long-term expertise and evaluation.

Together, these features reveal how legal design—not corporate intent alone—structures biodiversity neglect within CSR practice.

Biodiversity Law and CSR Law: A Structural Mismatch

The Biological Diversity Act, 2002 (BDA) conceptualises biodiversity as a sovereign national asset, governed through regulatory control, access restrictions, and benefit-sharing obligations. It prioritises conservation, equity, and accountability through mandatory Access and Benefit Sharing (ABS), prior approvals from the National Biodiversity Authority, and explicit corporate liability provisions.

By contrast, CSR law adopts a voluntary, partnership-based development framing, emphasising discretion and philanthropy. This divergence creates a regulatory gap- CSR-funded biodiversity restoration is not formally linked to ABS obligations or biodiversity governance structures.

Table 3: Quantitative Indicators of Biodiversity Law–CSR Governance Mismatch in India

| Indicator | Biodiversity Law (BDA Framework) | CSR Biodiversity Practice | Mismatch Gap (%) | Data Source Base |

|---|---|---|---|---|

| Projects requiring statutory approval | 100% (mandatory under BDA access/use cases) | ~15–20% CSR biodiversity projects seek NBA/SBB linkage | ~80% gap | NBA approvals vs CSR filings |

| Benefit-sharing obligation (ABS) | 100% mandatory where bio-resources are used | <10% CSR biodiversity projects are linked to ABS | ~90% gap | ABS fund records; CSR reports |

| Community institutional involvement (BMCs) | Statutorily required | ~20–25% CSR conservation projects involve BMCs | ~75% gap | State Biodiversity Boards |

| Ecological impact assessment requirement | Mandatory under biodiversity regulation | <30% CSR projects conduct biodiversity impact studies | ~70% gap | CSR sustainability reports |

| Liability for biodiversity damage | Civil & criminal penalties applicable | No direct CSR liability linkage | 100% structural gap | BDA enforcement vs CSR rules |

| Monitoring & audit mechanism | Statutory biodiversity monitoring | ~25–35% CSR projects have ecological audits | ~65% gap | Third-party audit disclosures |

| Benefit flows to local communities | ABS revenue-sharing mandated | ~30% CSR biodiversity funds reach local stewardship groups | ~70% gap | CSR implementation data |

Table 3. Figures are derived from aggregated review of CSR reports (2019–2024) and NBA approval records; represent indicative patterns rather than exhaustive national data.

CSR, ESG, and the Persistence of Symbolic Compliance

The BRSR framework has improved transparency, but continues to allow symbolic compliance through:

- Voluntary classification of biodiversity disclosures as “Leadership Indicators”;

- A persistent spending-centric compliance culture;

- Materiality assessment bias, favouring financial over ecological risks;

- “Comply or explain” flexibility that weakens accountability;

- Delayed value-chain disclosures, obscuring major biodiversity impacts;

- Persistent data constraints are undermining long-term planning.

Case Studies: CSR-Led Biodiversity Interventions in India

Here are some notable Corporate Social Responsibility (CSR) initiatives in India that engage with biodiversity conservation, habitat restoration, and species protection. Collectively, these cases indicate a gradual shift away from symbolic, input-focused activities (such as single-species plantation drives) toward more science-backed, outcome-oriented ecological interventions.

1. Reforestation and Habitat Restoration

CSR interventions under this category focus on restoring degraded land through multi-species plantations, agroforestry systems, and accelerated forest regeneration techniques. These projects primarily address carbon sequestration, soil regeneration, and local livelihood support, with biodiversity outcomes often emerging as secondary benefits.

- Mahindra – Project “Hariyali”: Over 20 million trees planted across multiple states, with an emphasis on native, multi-species plantations. The programme incorporates geo-tagging and third-party survival audits. In regions such as Araku, farmer training in micro-nursery management has integrated livelihood outcomes with ecological restoration.

- ITC – “Social and Farm Forestry”: Spanning over 1.2 million acres, this agroforestry model integrates fruit, fodder, and pulpwood species on degraded land. The approach improves soil health, diversifies farmer income, and secures raw material supply chains, while indirectly supporting landscape-level biodiversity.

- Tata Power – Western Ghats Initiatives (including “GhanVan”): Long-term plantation efforts, which exceed 18 million saplings, focus on spring rejuvenation and the restoration of indigenous species.

- GMDC–GVT – “Smritivan”: Using the Miyawaki method, dense native forests were established on arid land, achieving accelerated growth and rapid habitat formation. While biodiversity density increases are evident, the intervention remains primarily restorative.

2. Marine and Coastal Biodiversity (Blue Carbon)

Coastal CSR initiatives represent one of the strongest intersections between climate mitigation and biodiversity outcomes, particularly through mangrove restoration and species protection.

- JSW Foundation – “Mangrove Restoration”: Restoration of over 70 hectares of mangroves along the Maharashtra coast has enhanced shoreline protection and increased fish nursery density, illustrating tangible biodiversity co-benefits.

- Adani Ports (APSEZ): Commitments include mangrove afforestation and conservation exceeding 5,000 hectares, supported by water-efficient irrigation technologies. A dedicated corpus for Olive Ridley turtle protection near Dhamra Port marks a clearer orientation towards biodiversity protection.

- TCS – “Olive Ridley Turtle Conservation”: In partnership with NGOs, the project safeguards nesting sites, supports hatchery-based protection, and integrates eco-tourism as an alternative livelihood—representing a rare CSR model focused explicitly on species protection rather than habitat restoration alone.

3. Wildlife Rescue and Species Protection

This category reflects direct biodiversity protection, largely through rescue, rehabilitation, and population stabilisation of vulnerable species. These interventions are typically institution-heavy and geographically concentrated.

- Reliance Foundation – “Vantara”: One of the world’s largest wildlife rescue and rehabilitation centres, Vantara houses over 150,000 animals across 2,000+ species. With its unmatched scale, the model prioritises ex-situ conservation and welfare over ecosystem-level biodiversity protection.

- DB Corp – “Save Bird” Campaign: A mass-participation awareness initiative addressing urban bird mortality through distributed water and feed stations, representing low-cost, behaviour-oriented biodiversity support.

- HCL Foundation – “Harit”: Combines animal welfare, vaccination drives, and waterbody conservation, demonstrating an integrated—but impact-diffuse—approach.

4. Urban and Industrial Biodiversity Models

Several corporations have converted operational landholdings into functional micro-ecosystems, particularly in urban and industrial belts.

- Infosys – “Mysuru Campus”: Approximately 60% of the campus is maintained as native woodland and wetlands, supporting over 110 bird species. This represents a rare example of biodiversity integration within corporate infrastructure.

- Tata Motors – “Pune Wetland”: A 245-acre wetland within an industrial corridor functions as a habitat for migratory birds and contributes to local microclimate regulation.

- Tata Chemicals – “Mithapur Botanical Reserve”: A dedicated conservation zone supporting threatened species, including the Indian star tortoise, indicates movement toward site-specific biodiversity protection.

5. Circular Economy and Water Security (Indirect Biodiversity Outcomes)

While not biodiversity-focused per se, these CSR interventions reduce environmental pressure on ecosystems.

- Hindustan Unilever – Plastic Circularity: Processing over 1.2 million tonnes of post-consumer plastic has reduced terrestrial and marine pollution risks, with strong social co-benefits through waste-picker integration.

- Reliance Foundation – Water Security Programme: Revival of over 15,000 water harvesting structures using ridge-to-valley approaches has improved groundwater levels and indirectly supported surrounding ecosystems.

However, the planning and execution of these initiatives reveal a continued preference for restoration and rehabilitation over proactive biodiversity protection.

Interpreting Global Nature Disclosure Frameworks Across India’s Biodiversity-Intensive Industrial Economy

The emergence of the Corporate Sustainability Reporting Directive (CSRD) and the Taskforce on Nature-related Financial Disclosures (TNFD) signals a paradigmatic transition in corporate environmental governance—from expenditure-based sustainability to risk-accountable ecological stewardship. While global in regulatory design, these frameworks acquire particular analytical relevance when interpreted through India’s biodiversity-intensive industrial economy, where infrastructure expansion, extractive production, energy generation, and manufacturing growth intersect directly with ecologically sensitive landscapes.

India’s industrialisation trajectory spans forest regions, coastal zones, arid ecosystems, river basins, and tribal habitations. As a result, biodiversity risk is not sector-isolated but systemically distributed across multiple industries. Interpreting CSRD and TNFD through a multi-sector lens, therefore, offers a more accurate governance framework than extractive-sector analysis alone.

CSRD: Standardising Biodiversity Disclosure Across Industrial Sectors

Under the Corporate Sustainability Reporting Directive, biodiversity accountability is operationalised through the European Sustainability Reporting Standards (ESRS), particularly ESRS E4 (Biodiversity and Ecosystems). Applied to India’s industrial sectors, disclosure obligations would require corporations to report site-specific ecological impacts, dependencies, and mitigation strategies.

Sectoral Disclosure Exposure

- Mining & Metals: Forest land diversion; Habitat destruction in the lease areas; Overburden dumping and land degradation

- Energy (Thermal & Hydropower): Fly ash disposal impacts; Reservoir submergence of forests; River flow alteration and aquatic biodiversity loss.

- Infrastructure & Transport Corridors: Land fragmentation; Wildlife corridor disruption; Linear deforestation impacts

- Cement & Construction Materials: Limestone quarrying; Dust pollution; Karst ecosystem damage

- Ports & Coastal Industry: Mangrove clearance; Coastal erosion; Marine biodiversity disruption

Mitigation Hierarchy Enforcement

CSRD’s mitigation hierarchy—avoid, minimise, restore, offset—would require Indian corporations to demonstrate measurable ecological restoration rather than symbolic compensatory afforestation. Auditable restoration indicators would include plantation survival rates, soil regeneration capacity, species return indices, and wetland and watershed recovery metrics. Thus, biodiversity governance transitions from narrative CSR reporting into audited ecological performance disclosure.

TNFD: Embedding Nature Risk Within Industrial Finance

While CSRD mandates disclosure, TNFD embeds biodiversity within financial risk governance. Its four-pillar architecture—Governance, Strategy, Risk & Impact Management, Metrics & Targets—requires corporations to integrate nature into enterprise risk systems.

Across India’s industrial economy, nature dependency manifests through land acquisition from forest ecosystems, freshwater extraction for industrial processing, energy dependence on coal and hydrological systems, coastal and marine ecosystem utilisation, and biomass and agricultural raw material sourcing.

Sectoral Nature-Related Financial Risks

- Regulatory Exposure: Environmental penalties, clearance delays, and biodiversity offset liabilities.

- Operational Disruption: Resource scarcity, ecosystem collapse, supply chain interruptions.

- Social Conflict: Tribal land resistance, livelihood displacement movements.

- Financial Market Risk: ESG rating downgrades, investor withdrawal, and insurance premiums.

TNFD, therefore, reframes biodiversity degradation as balance-sheet exposure rather than reputational concern.

Applying the LEAP Framework Across India’s Industrial Landscape

The LEAP methodology enables structured biodiversity risk mapping across sectors.

Locate

Industrial operations overlap with forests, wetlands, coastal belts, agricultural zones, and biodiversity hotspots.

Evaluate

Impacts include deforestation, hydrological alteration, particulate pollution, marine degradation, and habitat fragmentation.

Assess

These impacts generate material risks—litigation exposure, stranded assets, restoration liabilities, and social license erosion.

Prepare

Strategic responses would require biodiversity management systems, ecosystem restoration financing, and science-based transition planning.

At the national scale, implementation challenges include fragmented ecological datasets, limited corporate geospatial disclosure, and weak integration between environmental clearance and financial reporting systems.

Disclosure vs. Industrial Ecological Reality

Corporate sustainability reporting in India has historically prioritised the following climate-centric metrics:

- Carbon emission reductions.

- Renewable energy transitions.

- Energy efficiency gains.

While significant, these disclosures often obscure localised biodiversity degradation within host ecosystems. CSRD and TNFD address this imbalance by mandating location-specific ecological risk mapping, habitat disturbance disclosure, species impact accounting, and ecosystem dependency valuation. This prevents the substitution of global carbon performance for local biodiversity accountability.

Convergence with India’s CSR Architecture

India’s CSR regime provides a statutory financial pipeline for environmental action but remains expenditure-oriented rather than impact-calibrated. Integrating CSRD and TNFD analytics could transform CSR governance through biodiversity risk-linked CSR allocation, LEAP-based project prioritisation, site-level ecological audit mandates, and restoration outcome disclosure integration. Such convergence would align corporate spending with scientifically assessed ecological risk geographies.

Towards a Nature-Accountable Industrial Economy

As India expands infrastructure, manufacturing, and extractive production, biodiversity governance will increasingly shape regulatory legitimacy, investor confidence, and community acceptance.

CSRD provides the disclosure architecture; TNFD supplies the risk analytics. Applied across India’s industrial sectors, these frameworks enable a transition from symbolic environmentalism to measurable ecological stewardship. In this governance evolution, biodiversity ceases to be a peripheral CSR theme and instead becomes a core determinant of industrial financial resilience, regulatory compliance, and long-term sustainability.

Justiciable Biodiversity Responsibility and Corporate Accountability: The Great Indian Bustard Judgment (2025)

In M.K. Ranjitsinh & Ors. v. Union of India & Ors., Writ Petition (Civil) No. 838 of 2019 (Supreme Court of India, December 2025), the Supreme Court of India significantly expanded the jurisprudential interface between biodiversity protection and corporate accountability. The proceedings arose from a Public Interest Litigation filed under Article 32 of the Constitution seeking urgent protection of the critically endangered Great Indian Bustard (GIB) across Rajasthan and Gujarat. Owing to the ecological complexity and regulatory implications of the matter, the Court adopted a continuing mandamus approach, retaining supervisory jurisdiction and issuing periodic compliance directions relating to habitat protection and power transmission infrastructure.

In its December 2025 ruling, the Court brought ecological protection within the enforceable ambit of Corporate Social Responsibility (CSR). Departing from the conventional understanding of CSR as discretionary or reputational expenditure, the Court reframed biodiversity protection as a constitutional obligation grounded in Articles 21 and 51A(g) of the Constitution. Article 51A(g) imposes a fundamental duty upon every citizen to protect and improve the natural environment; the Court reasoned that corporate entities, as juristic persons operating within environmentally sensitive geographies, cannot remain insulated from this constitutional ethic.

The judgment marks a doctrinal shift in Indian environmental jurisprudence. By reading Article 51A(g) in conjunction with the expanded environmental dimension of Article 21 (right to life), the Court elevated biodiversity protection from policy aspiration to enforceable constitutional responsibility. Corporate environmental expenditure—particularly in ecologically fragile zones—was thus characterised not as voluntary philanthropy but as compliance with constitutional environmental obligations.

This interpretive expansion effectively constitutionalises environmental CSR. It embeds ecological stewardship within the enforceable duties of corporate actors whose commercial operations intersect with biodiversity-rich landscapes. In doing so, the Court signalled a transition from charity-based CSR toward justiciable ecological accountability, aligning corporate conduct with India’s evolving environmental constitutionalism.

The “Guest in the Abode” Doctrine

One of the most jurisprudentially significant elements of the judgment is the Court’s directive that power generation and transmission companies operating within GIB habitats must conduct their commercial activities “as if they are guests in the abode” of the species. This ecological metaphor operationalises the public trust doctrine within corporate conduct, positioning industry not as sovereign users of land but as conditional occupants within shared ecological habitats.

The doctrine establishes three normative expectations:

- Heightened ecological sensitivity in project planning and execution.

- Habitat coexistence obligations rather than mere regulatory compliance.

- Restorative responsibility where industrial activity disrupts biodiversity.

The “guest” formulation thus transforms environmental compliance from a procedural clearance requirement into a substantive obligation of ecological sensitivity. It signals that industrial development in conservation zones is constitutionally permissible only to the extent that it does not compromise species survival or habitat continuity.

Importantly, this articulation extends beyond the immediate GIB context. The reasoning potentially applies to all corporate operations situated within forests, grasslands, wetlands, coastal ecosystems, and other biodiversity-sensitive geographies. By embedding habitat respect within constitutional environmental jurisprudence, the Court has strengthened the doctrinal bridge between environmental fundamental duties and corporate governance responsibilities.

In effect, the “Guest in the Abode” doctrine advances India’s environmental constitutionalism by integrating biodiversity protection, industrial regulation, and CSR accountability within a unified normative framework. Industrial activity is no longer assessed solely against statutory compliance benchmarks, but against a higher constitutional standard of ecological coexistence.

Spatial Governance and Conservation Zoning

The Court accepted the recommendations of a specialised expert committee and approved revised priority conservation areas covering 14,013 sq km in Rajasthan and 740 sq km in Gujarat.

These designated landscapes were recognised as critical habitats requiring focused protection and industrial regulation. By judicially endorsing conservation zoning, the Court effectively merged biodiversity science with enforceable land-use governance.

Renewable Energy–Biodiversity Conflict

The judgment is particularly significant in addressing the ecological externalities of renewable energy expansion. While solar and wind infrastructure is central to India’s climate transition, the Court acknowledged that large-scale deployment has frequently encroached upon arid grasslands and scrub ecosystems that constitute primary habitats of the GIB. Key ecological risks identified include collision mortality from overhead transmission lines, habitat fragmentation from solar arrays, disturbance of breeding and foraging grounds, and landscape-scale alteration of grassland ecology. This recognition disrupts the policy assumption that renewable energy infrastructure is ecologically benign, introducing biodiversity accountability within climate mitigation projects.

Regulatory Directions to Industry

To mitigate biodiversity harm, the Court issued binding operational directives, including:

- A blanket prohibition on solar installations above 2 MW capacity within designated conservation zones;

- A ban on overhead transmission lines in priority habitats;

- Mandatory undergrounding of power lines in ecologically sensitive areas.

These directions significantly increase infrastructure costs but embed biodiversity risk into project feasibility calculations—effectively internalising ecological externalities within industrial finance.

Corporate Compliance and Technological Adaptation

In response to judicial mandates, several energy corporations have initiated mitigation interventions. These include:

- Installation of avian bird diverters on transmission lines;

- Deployment of flagged poles and line markers to improve visibility;

- Habitat-sensitive infrastructure routing.

Monitoring data from pilot landscapes indicates that bird diverters have contributed to approximately 70% reduction in collision mortality in certain transmission corridors. While not substitutes for undergrounding, these technologies represent interim biodiversity risk mitigation tools.

Corporate Conservation Partnerships

Beyond compliance measures, some corporations have initiated biodiversity-positive CSR programmes aligned with the Court’s ecological accountability logic. Notable initiatives include adoption and ecological restoration support for protected habitats, grassland regeneration projects, and community-linked conservation funding. For instance, corporate participation in conservation support for sites such as the Rollapadu Wildlife Sanctuary reflects an emerging model where CSR finances habitat restoration rather than peripheral welfare activities.

Doctrinal Implications for CSR Governance

The Great Indian Bustard judgment produces three structural transformations in CSR jurisprudence:

- From Voluntary to Justiciable CSR: Environmental CSR may now be subject to judicial review where ecological harm persists.

- From Expenditure to Impact Accountability: Spending must demonstrate biodiversity outcomes, not merely financial allocation.

- From Peripheral Welfare to Core Ecological Restitution: CSR must correspond to operational ecological externalities.

Convergence with Global Disclosure Frameworks

The ruling also aligns structurally with global nature disclosure regimes such as CSRD and TNFD.

Table 4: Comparison of CSRD and TNFD Frameworks

| Judicial Doctrine | CSRD Link | TNFD Link |

|---|---|---|

| Habitat disclosure | ESRS E4 site-level reporting | LEAP “Locate” |

| Biodiversity risk | Impact disclosure | Risk & impact management |

| Restoration mandates | Mitigation hierarchy | Nature transition planning |

| Financial internalisation | Sustainability reporting | Balance-sheet risk |

Thus, Indian constitutional jurisprudence is converging with transnational biodiversity disclosure norms, embedding ecological accountability simultaneously within law, finance, and corporate governance.

Constitutionalising Biodiversity Governance

The GIB judgment marks a watershed moment in India’s environmental rule of law. By framing biodiversity protection as a constitutional duty enforceable through CSR obligations, the Supreme Court has reclassified corporate environmental responsibility from symbolic compliance to justiciable ecological stewardship. The “guest in the abode” doctrine, conservation zoning mandates, renewable energy regulation, and restoration-linked CSR collectively signal the emergence of a jurisprudence where industrial development is conditional upon biodiversity coexistence.

In governance terms, the ruling bridges three accountability regimes- constitutional environmental duties, corporate sustainability governance, and global nature disclosure frameworks. Together, these shifts position biodiversity not as an externality of industrial growth but as a central determinant of corporate legitimacy within India’s ecological constitutional order.

Comparative Insights: Lessons for India

The structure of corporate responsibility for environmental and biodiversity concerns differs markedly between India and selected European jurisdictions (here, the UK, France, and Germany), reflecting divergent regulatory philosophies. While India relies on a mandatory CSR spending model, the UK, France, and Germany embed biodiversity concerns within corporate governance, due diligence, and risk management frameworks. This distinction has significant implications for the depth and durability of corporate engagement with biodiversity protection.

India: CSR as Post-Profit Expenditure

Although biodiversity is not consistently articulated as a standalone objective, Schedule VII of the Companies Act, 2013 explicitly covers environmental sustainability, ecological balance, protection of flora and fauna, and agroforestry, allowing biodiversity-related interventions to qualify as CSR. However, the framework conceptualises responsibility primarily as financial allocation, monitored through board-level CSR committees, rather than as an ongoing obligation integrated into business operations or risk governance. As a result, biodiversity conservation in India’s CSR ecosystem often remains project-based, peripheral, and discretionary, with limited linkage to corporate decision-making or long-term ecological outcomes.

France: Mandatory Due Diligence and Legal Accountability

France departs sharply from the Indian model through its Duty of Vigilance Law (2017), which requires large companies to identify, prevent, and mitigate environmental and biodiversity-related harms across their operations and supply chains. Here, corporate responsibility is framed not as spending, but as legal duty and risk prevention. Biodiversity concerns are embedded within vigilance plans, enforceable through judicial oversight and civil liability. Companies are expected to demonstrate proactive governance rather than post-hoc philanthropy.

Transferable insight for India here is that India could adapt elements of France’s approach by introducing mandatory environmental and biodiversity due diligence obligations, particularly for high-impact sectors, without dismantling the existing CSR spending framework. This would shift biodiversity from an optional CSR theme to a governance obligation.

Germany: Supply Chain Due Diligence and Preventive Responsibility

Germany’s Supply Chain Due Diligence Act similarly embeds environmental and biodiversity responsibilities into corporate governance structures. Companies are required to identify and address environmental risks, including those affecting ecosystems and natural resources, throughout their supply chains. Unlike India’s output-focused CSR model, Germany’s framework emphasises preventive responsibility, continuous monitoring, and corrective action. Biodiversity protection is approached indirectly, but systematically, as part of environmental risk management rather than isolated conservation projects.

Transferable insight for India here is that Germany’s model suggests a pathway for integrating biodiversity considerations into corporate risk assessment and supply chain governance, complementing India’s CSR regime by encouraging companies to address ecological harm upstream.

United Kingdom: Disclosure, Risk Governance, and Strategic Integration

The UK adopts a distinct approach centred on transparency, disclosure, and governance, rather than direct mandates for spending or due diligence. Through mechanisms such as mandatory non-financial reporting and emerging nature-related risk disclosures, companies are expected to identify and communicate their environmental and biodiversity risks. Biodiversity is treated as a material risk and dependency, influencing strategic decision-making rather than being confined to corporate philanthropy. While the UK framework remains less prescriptive than those of France or Germany, it encourages internalisation of ecological considerations within corporate strategy.

Transferable insight for India here is that India could strengthen its CSR framework by aligning CSR and BRSR disclosures more explicitly with biodiversity impact and dependency reporting, enabling a shift from activity reporting to impact-oriented accountability.

Comparative Insight and Relevance for India

Across France, Germany, and the UK, a common pattern emerges- biodiversity is embedded within corporate governance systems, rather than addressed solely through discretionary spending. In contrast, India’s CSR framework externalises ecological responsibility by locating it predominantly in post-profit CSR activities. The comparative evidence suggests that strengthening India’s CSR framework does not require abandoning its mandatory spending model, but rather supplementing it with governance-based mechanisms—including due diligence, risk disclosure, and policy alignment with national biodiversity objectives. Such integration would allow CSR to evolve from a compliance-driven expenditure obligation into a strategic instrument for biodiversity protection.

Findings and Analysis

1. Normative Commitment vs. Institutional Integration

The analysis reveals a clear normative acknowledgement of biodiversity within India’s CSR and environmental governance architecture. Policy instruments such as the Companies Act–mandated CSR framework, the National Guidelines on Responsible Business Conduct (NGRBC), and biodiversity legislation articulate ecological responsibility as a corporate obligation. However, biodiversity remains institutionally peripheral in corporate decision-making. It is referenced rhetorically but not embedded within capital allocation frameworks, risk assessment models, or board-level strategy. CSR spending patterns indicate that ecological concerns are treated as discretionary rather than systemic responsibilities. This gap reflects a broader structural tension: while environmental protection is legally recognised, biodiversity protection is not operationalised as a core business risk.

2. Restoration Bias in CSR Spending

A dominant trend emerging from case studies and CSR disclosures is the preference for restoration over protection. The observed pattern includes activities such as tree plantation drives, habitat restoration projects, water body rejuvenation, and afforestation-linked carbon initiatives. These interventions are output-friendly, visibly measurable, publicly communicable, and easier to align with Schedule VII of the Companies Act, 2013. In contrast, biodiversity protection—such as species monitoring, ecosystem preservation, or long-term conservation partnerships—receives comparatively limited funding.

Restoration aligns more comfortably with compliance structures, short CSR timelines, and reputation management goals. Protection, by contrast, requires long-term ecological monitoring and involves complex stakeholder coordination, yet yields less immediate reputational visibility. Thus, biodiversity is often framed as a co-benefit rather than a primary objective.

3. Concentration of High-Impact Biodiversity Projects

Large conglomerates with significant capital reserves and land access are more likely to undertake ambitious biodiversity initiatives. Smaller firms tend to outsource CSR projects by supporting existing NGOs to focus on low-cost, high-visibility environmental activities. This concentration produces inequality in biodiversity investment capacity across corporate India. Biodiversity leadership is, therefore, not systemic but concentrated among select entities.

4. Weak Impact Measurement and Ecological Verification

A major structural weakness is the absence of biodiversity-specific metrics in CSR reporting. Findings from ESG and CSR Reports include:

- Reliance on narrative reporting

- Limited ecological baselines

- Absence of species-level indicators

- No standardised biodiversity index integration

Most CSR disclosures measure funds allocated, area restored, and beneficiaries reached. Rarely do they measure the species recovery rates, habitat connectivity, and ecosystem resilience indicators. This indicates a compliance-driven reporting culture rather than outcome-oriented ecological accountability.

5. Geographical and Planning Disconnect

CSR spending is geographically concentrated to industrial zones, corporate operational regions, and politically-visible districts. Ecologically fragile regions often remain underfunded. Further, CSR projects operate largely independently of district-level biodiversity action plans and State Biodiversity Boards. The lack of vertical integration between corporate CSR and statutory conservation planning weakens long-term ecological coherence.

6. Legal and Structural Design Constraints

The mandatory 2% CSR expenditure model incentivises annual spending cycles, short-term disbursement pressures, and project fragmentation. There are limited incentives for multi-year biodiversity commitments, ecological risk disclosure, and alignment with biodiversity law enforcement. Without recalibrating timelines, incentives, and disclosure mandates, CSR remains structurally tilted toward symbolic compliance.

7. Strategic Reframing: Biodiversity as Risk Governance

The most significant analytical insight is conceptual- biodiversity is still treated as a philanthropic responsibility and a tool to maintain reputation. It is not treated as a supply chain risk or a financial stability concern. For CSR to meaningfully confront environmental neglect, biodiversity must shift from an ethical narrative to a corporate ecological risk management function integrated into board-level strategy and ESG decision-making.

Synthesis

India’s CSR architecture has evolved beyond pure philanthropy and demonstrates movement toward impact-oriented environmental engagement. However, the following concerns remain:

- Restoration dominates over protection.

- Measurement remains weak.

- Institutional integration is limited.

- Biodiversity remains structurally under-prioritised.

The core issue is not the absence of intent but design misalignment. Until biodiversity protection is embedded into corporate governance structures—through legal recalibration, risk-based disclosure frameworks, and ecological metrics—CSR will struggle to deliver transformative conservation outcomes.

Reimagining CSR Beyond the 2% Rule

Corporate Social Responsibility (CSR) in India is undergoing a structural shift from a philanthropic welfare orientation to a strategic ecological stewardship approach. Within this transformation, biodiversity conservation has emerged as a critical yet underfinanced domain. Although India is one of the world’s megadiverse countries and corporate operations significantly intersect with ecological landscapes, biodiversity continues to receive disproportionately low CSR attention.

A major concern identified is the biodiversity financing gap within CSR allocation structures. Current expenditure trends indicate that biodiversity conservation accounts for only 2–3% of total CSR spending, reflecting an institutional preference for social development sectors such as education and healthcare. This underinvestment persists despite escalating biodiversity loss, ecosystem degradation, and climate-linked habitat risks.

Regulatory developments, however, are beginning to reconfigure corporate biodiversity engagement. The introduction of the Business Responsibility and Sustainability Reporting (BRSR) Framework that mandates the top 1,000 listed companies to disclose environmental externalities, including impacts on ecologically sensitive zones, protected forests, and biodiversity-rich regions, is expanding corporate accountability from financial performance to ecological footprint assessment.

Further reinforcing this shift, India’s updated National Biodiversity Strategy and Action Plan (NBSAP) 2024–2030 explicitly emphasises private sector participation in biodiversity financing. The policy framework calls for integration of biodiversity considerations into corporate risk assessment, supply chain governance, and long-term sustainability planning. Together, these regulatory drivers signal a transition from voluntary biodiversity philanthropy to compliance-linked ecological governance.

From a sectoral perspective, biodiversity pressures are not uniformly distributed across industries. High-impact sectors demonstrate disproportionately large ecological footprints. As shown in Table 4, the food and staple retail sector contributes the highest share to global species richness loss, accounting for 44.5% of Potentially Disappeared Function (PDF), followed by materials (31.7%) and industrials (13.7%). These sectors drive biodiversity loss through land-use change, extractive sourcing, infrastructure expansion, and supply chain intensification.

Table 5: Sectoral Impact on Global Species Richness (PDF Index)

| Industrial Sector | Potentially Disappeared Function (PDF) |

|---|---|

| Food & Staple Retail | 44.5% |

| Materials | 31.7% |

| Industrials | 13.7% |

| Real Estate Services | 2.6% |

| Healthcare | 0.3% |

Despite these high sectoral impacts, CSR allocation remains misaligned. As illustrated in Table 5, education and skill development command 44% of CSR expenditure, while healthcare and water, sanitation, and hygiene (WASH) account for 29%. Environmental sustainability receives only 10%, within which biodiversity forms a very small subset at 2–3%. This structural imbalance underscores the urgency of reimagining CSR priorities toward ecological regeneration.

Table 6: The Biodiversity Gap in National CSR Allocation (FY 2023–24)

| Sector | % Share of Total CSR | Primary Thematic Focus |

|---|---|---|

| Education & Skills | 44% | Literacy, schools, vocational training |

| Healthcare & WASH | 29% | Hospitals, sanitation, maternal care |

| Environment/Sustainability | 10% | Energy, waste, emissions |

| Biodiversity Conservation | 2–3% | Wildlife, mangroves, habitat restoration |

Five priority pathways have been identified through which CSR can meaningfully contribute to biodiversity outcomes. These include wildlife habitat conservation, development of urban biodiversity parks (such as Bannerghatta National Park, Bengaluru and Sanjay Gandhi National Park, Mumbai), mangrove ecosystem restoration, rural biodiversity stewardship, and promotion of sustainable agriculture systems. Such interventions not only restore ecosystems but also generate co-benefits, including carbon sequestration, livelihood security, and climate resilience.

Reimagining Sustainability: Circular Economy and Climate Resilience

Beyond biodiversity, CSR sustainability discourse in India is expanding toward circular economy transitions and climate adaptation financing. Corporations are increasingly recognising that environmental responsibility is not merely reputational but operationally strategic. The circular economy model represents a fundamental departure from the linear “take–make–dispose” production system. Corporate initiatives in recycling, material recovery, and waste valorisation demonstrate how sustainability can generate both ecological and financial returns. Large-scale PET recycling and plastic recovery programs exemplify how industrial waste streams can be reintegrated into production cycles.

Simultaneously, climate resilience is becoming embedded within CSR frameworks. Approximately 75% of Indian corporations report plans to integrate climate adaptation strategies into CSR programming. These include watershed restoration, drought mitigation, flood-resilient infrastructure, and community-based climate preparedness initiatives. CSR, thus, functions as a decentralised financing instrument supporting India’s broader climate adaptation architecture.

Technological innovation is further accelerating sustainability reimagination. Artificial Intelligence is being deployed for biodiversity mapping and resource optimisation; blockchain systems enhance supply chain traceability and carbon credit verification; IoT-enabled sensors support real-time emissions monitoring and waste tracking. Such technologies improve transparency, accountability, and ESG reporting precision.

Afforestation strategies are also evolving scientifically. The Miyawaki method, involving dense plantation of native species, is gaining corporate traction due to its rapid growth rates, high carbon absorption capacity, and suitability for urban micro-forests.

CSR spending patterns within environmental sustainability reflect these evolving priorities. As shown in Table 6, renewable energy commands the largest share (30%), followed by water conservation (20%) and climate technology investments (25%).

Table 7: Allocation within Environmental CSR (FY 2023)

| Category | CSR Spending (₹ Crore) | % of Environmental Budget |

|---|---|---|

| Renewable Energy | 3,600 | 30% |

| Water Conservation | 2,400 | 20% |

| Waste & Recycling | 1,800 | 15% |

| Afforestation | 1,200 | 10% |

| Climate Tech / AI / Other | 3,000 | 25% |

Corporate Case Studies for Benchmarking Nature-Positive CSR

Empirical corporate initiatives provide measurable benchmarks for evaluating CSR effectiveness in biodiversity and sustainability domains. Large-scale afforestation programs demonstrate significant carbon sequestration potential, while industrial water stewardship projects highlight how CSR can address hydrological stress. Renewable energy transitions reflect corporate alignment with decarbonization pathways, and plastic waste recovery initiatives illustrate circular economy scalability.

Table 8: Benchmarking Nature-Positive CSR Models

| Company | Project | Measurable Impact | SDG Alignment |

|---|---|---|---|

| Mahindra | Project Hariyali | 22 million trees; 3.9 lakh tonnes carbon sequestered | SDG 13, 15 |

| Reliance | PET Recycling | 2.2 billion bottles recycled annually | SDG 12 |

| ITC Ltd. | Water Stewardship | 1 million acres revitalised; 15,000 structures | SDG 6 |

| Tata Power | Clean Energy | 3,600 MW renewable capacity; 4.5M tCO₂ reduced | SDG 7, 13 |

| HUL | Plastic Waste Management | 100,000 tonnes of plastic are recycled annually | SDG 12 |

Future Trajectory of CSR Financing (2025–2035)

CSR expenditure in India is projected to expand exponentially over the coming decade, positioning corporate finance as a parallel pillar to public development spending. Forecast models estimate annual CSR spending to reach ₹38,000 crore by 2025, rising to ₹60,000 crore by 2030, and surpassing ₹1.2 lakh crore by 2035. Growth drivers include regulatory expansion, digital transparency mandates, ESG compliance pressures, and rising corporate profitability.

Table 9: CSR Expenditure Forecast — Road to 2035

| Year | Projected Annual CSR Spending | Strategic Driver |

|---|---|---|

| 2025 | ₹38,000 Crore | Inclusion of mid-size firms |

| 2028 | ₹45,000 Crore | Digital CSR transparency |

| 2030 | ₹60,000 Crore | Net-Zero policy alignment |

| 2035 | ₹1,20,000 Crore | GDP growth & profit expansion |

Analytical Synthesis

The reimagining of CSR in India reflects a paradigmatic evolution from philanthropic obligation to sustainability governance infrastructure. Biodiversity conservation, circular economy transitions, and climate resilience financing are emerging as the three defining pillars of next-generation CSR. However, the persistence of the biodiversity funding gap indicates that ecological priorities remain structurally marginalised within corporate giving frameworks. Bridging this gap will require regulatory deepening, disclosure standardisation, sector-specific biodiversity mandates, and integration of nature-related risk into corporate financial decision-making. As CSR financial volumes expand toward 2035 projections, the strategic allocation of these resources will determine whether corporate India can transition from being a driver of ecological degradation to a catalyst of planetary restoration.

Conclusion

This study has examined the evolving role of Corporate Social Responsibility (CSR) in addressing biodiversity loss and ecological degradation in India, moving beyond compliance-based spending toward strategic environmental stewardship. The findings reveal that while Section 135 and Schedule VII of the Companies Act, 2013 have created a mandatory financial architecture for CSR, biodiversity protection remains under-prioritised relative to more visible restoration and philanthropic activities. Corporate engagement is largely project-based, fragmented, and often disconnected from measurable ecological outcomes.

The analysis demonstrates that biodiversity conservation through CSR is both legally permissible and operationally feasible, particularly when aligned with national priorities such as the National Biodiversity Action Plan, protected area management, and international commitments under the Convention on Biological Diversity and the Sustainable Development Goals, particularly SDGs 11 (Sustainable Cities and Communities), 13 (Climate Action), 14 (Life below Water), and 15 (Life on Land). However, current interventions frequently emphasise afforestation and habitat restoration without integrating long-term ecosystem protection, scientific monitoring, or landscape-level planning.

The study concludes that India’s CSR regime possesses significant untapped potential to support biodiversity protection, provided that regulatory clarity, standardised impact metrics, transparency in reporting, and alignment with ESG and emerging frameworks such as TNFD are strengthened. Reimagining CSR as a mechanism for ecological and ethical responsibility—rather than reputational compliance—can enable corporations to become meaningful contributors to biodiversity resilience and sustainable development.

Limitations of the Study

While the present study attempts to provide a comprehensive re-examination of Corporate Social Responsibility (CSR) beyond the statutory 2% mandate by integrating biodiversity and sustainability perspectives within the Indian context, certain methodological, data-related, and structural limitations must be acknowledged.

First, the study relies significantly on secondary data drawn from corporate disclosures, sustainability reports, Business Responsibility and Sustainability Reports (BRSR), CSR portals, and regulatory filings. Although these sources are authoritative, they are inherently dependent on self-reporting by corporations. This creates the possibility of reporting bias, selective disclosure, and inconsistencies in biodiversity-related expenditure classification. Many companies aggregate environmental spending under broad sustainability heads, making it difficult to isolate biodiversity-specific CSR investments with precision.

Second, the quantitative analysis is constrained by data availability and accessibility. Government databases and official CSR repositories often present incomplete, delayed, or non-standardised datasets. Variations in reporting formats across financial years further limited longitudinal comparability. As a result, trend analysis of biodiversity funding within CSR expenditure had to rely on estimations, proxy indicators, and triangulation from multiple sources rather than a single unified dataset.

Third, biodiversity remains an under-defined category within India’s CSR framework. Schedule VII of the Companies Act provides broad environmental categories but does not mandate granular biodiversity reporting. This regulatory ambiguity limits the ability to construct sector-wise or ecosystem-specific funding comparisons, thereby affecting the depth of quantitative disaggregation.

Fourth, the qualitative component of the study—comprising literature review, policy analysis, and interpretive assessment of global disclosure frameworks such as CSRD and TNFD—introduces interpretive subjectivity. While efforts were made to rely on peer-reviewed literature, policy documents, and institutional reports, the forward-looking nature of sustainability governance means that some frameworks are still evolving. Their projected applicability to India may therefore differ in practice from current theoretical expectations.

Fifth, the study adopts a macro-institutional perspective focusing on regulatory evolution, financial flows, and disclosure architecture. Consequently, it does not incorporate extensive primary fieldwork, stakeholder interviews, or community-level biodiversity impact assessments. The absence of ground-level project evaluation limits the ability to measure ecological outcomes vis-à-vis reported CSR spending.

Sixth, sectoral representation presents another limitation. Industries with high disclosure maturity—such as mining, metals, energy, and heavy manufacturing—are overrepresented in CSR biodiversity reporting, whereas MSMEs and unlisted entities remain underexplored due to limited public disclosures. This skews the analytical lens toward large corporations.

Seventh, temporal limitations must be noted. CSR as a regulated mandate in India is barely more than a decade old, and biodiversity integration within CSR is an even more recent phenomenon. Therefore, long-term impact assessment—particularly ecological regeneration, species recovery, or habitat restoration—falls outside the measurable scope of the present dataset.

Finally, the study is situated within the Indian regulatory and institutional ecosystem. While it draws comparative insights from global frameworks, the findings may not be fully generalizable to other jurisdictions with different CSR mandates, disclosure regimes, or biodiversity governance structures.

Scope of the Study

This study explores the transformation of Corporate Social Responsibility (CSR) in India beyond its statutory 2% expenditure mandate, repositioning CSR as a strategic governance and financing mechanism for biodiversity conservation and sustainability transitions. The research is situated within the Indian regulatory and institutional context and examines how corporate environmental responsibility is being reshaped through evolving policy mandates, disclosure frameworks, and sustainability expectations.

The analytical scope combines quantitative and qualitative approaches. On the quantitative front, the study evaluates CSR expenditure trends from the post-mandate period (2014 onwards), with particular attention to the scale, growth, and thematic allocation of funds toward environmental sustainability and biodiversity-related initiatives. These include afforestation, habitat restoration, wildlife protection, watershed development, and ecosystem regeneration programs.

Qualitatively, the study assesses the policy and disclosure architecture influencing biodiversity integration within CSR. It reviews national reporting requirements alongside emerging global sustainability frameworks to understand their implications for corporate nature-related accountability, risk disclosure, and strategic alignment.

Sectorally, the research focuses on environmentally intensive industries—such as mining, metals, energy, and heavy manufacturing—where ecological externalities are significant, and CSR intervention potential is substantial. The study evaluates whether CSR investments in these sectors correspond proportionately to their environmental footprints.

While the research analyses financial flows, governance structures, and disclosure evolution, it does not extend to primary field-based biodiversity impact assessments or ecological outcome measurement at the project level.

References

- 10 Green CSR projects by Indian companies

- 7 CSR Projects Changing India’s Environmental Future: An Earth5R Insight

- Addison, P. F. E., Bull, J. W. and Milner-Gulland, E. J. (2019). Using conservation science to advance corporate biodiversity accountability. Conservation Biology, 33(2), 307–318. https://doi.org/10.1111/cobi.13190

- Bansal S., Jiang G. F., Jung J. C. (2015). Mandatory CSR in India: Compliance or Commitment? Journal of Corporate Law Studies, 15(2), 259–286. https://doi.org/10.1016/j.lrp.2014.07.002

- Chatterjee, B., Mitra, N. CSR should contribute to the national agenda in emerging economies – the ‘Chatterjee Model’. Int J Corporate Soc Responsibility 2, 1 (2017). https://doi.org/10.1186/s40991-017-0012-1

- Contribution of GMDC-GVT to Dense Forestation through Miyawaki Plantation at Smritivan, Earthquake Memorial, Bhujiyo Dungar, Kachchh

- Dashwood, H. S. (2012). The rise of global corporate social responsibility: Mining and the spread of global norms. Cambridge University Press. https://doi.org/10.1017/CBO9781139058933

- Dharmapala, D., & Khanna, V. (2018). The impact of mandated corporate social responsibility: Evidence from India’s Companies Act of 2013. International Review of Law and Economics, 56, 92–104. https://doi.org/10.1016/j.irle.2018.09.001

- Eccles, R. G., & Klimenko, S. (2019). The investor revolution. Harvard Business Review, 97(3): 106–116.

- Environment | Tata and the community

- Environmental Sustainability through CSR Initiatives – Kushaagra Innovations Foundation

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman. https://doi.org/10.2139/ssrn.263511

- Ganesh, M. K., & Venugopal, B. (2024). Challenges, practice and impact of corporate social responsibility on sustainable development of environment and society. Revista De Gestão Social E Ambiental, 18(1), 1-13. https://doi.org/10.24857/rgsa.v18n1-067

- Gardens Of Green | Tata Group

- Garg P., Gupta A, Kumar V. (2020). CSR expenditure and environmental sustainability in India. Social Responsibility Journal, 16(7), 969–983. https://doi.org/10.28992/ijsam.v5i1.338

- Ghanvan

- Gunningham, N., and Kagan, R. A., & Thornton, D. (2004). Social license and environmental protection. Law and Social Inquiry, 29(2), 307–341. https://doi.org/10.1086/423681

- Harit | HCLFoundation