ESG Reporting- history, present and future- A comparative study of India and United States

Created By-

- Sarvesh Akolkar | LinkedIn

- Rubin Cyriac | linkedln

- Kriti Kharwar | LinkedIn

- Kratika Soni | LinkedIn

- Bernadette I. Foroma | LinkedIn

Abstract-

ESG reporting constitutes that branch of corporate transparency that grants stakeholders access to a company’s sustainability and governance practices. ESG reporting entered the scene as a voluntary initiative. Still, with time and under immense investor pressure, well-acknowledged climate change issues, and a more accountable corporate environment, it has increasingly become a regulatory requirement in different parts of the world.

The study elaborates on the whole cycle of development of ESG reporting, regulatory frameworks, and adoption trends worldwide with a focused comparison between India and the United States (U.S.). It elaborates on the efficiency, perseverance, and evolution of ESG frameworks concerning both countries and presents trend analyses comparing India, the U.S., and the global average. Additionally, the study determines whether ESG reporting is a transformational tool or a facade for corporate greenwashing.

Finally, the paper highlights the impending challenges, required reforms, and forecasts about global ESG reporting.

Introduction

Within two decades, ESG reporting has emerged as one of the main instruments for the analysis of corporate sustainability. It has grown from an endeavor through corporate social responsibility into an almost regulatory requirement. Investors, governments, and consumers have all increasingly sought to hold corporations accountable, so the establishment of standardized ESG reporting frameworks came into being.

The growth of ESG frameworks has mainly been due to:

Demand from investors or types of investments that are ESG-linked (e.g., green bonds, sustainability-linked loans).

Regulations that require transparency from corporations about sustainability.

Public pressure and activism force companies to behave responsibly towards the environment and society.

However, ESG reporting parameters are different in different countries. This study traces the historical evolution of ESG reporting worldwide, then compares India with the U.S., and ultimately concentrates on the relevance, impact, and future aspects of ESG reporting.

History and Development of ESG Reporting

The environment, social, and governance (ESG) principles have evolved through many historical events, and the advancement of regulatory and corporate initiatives has focused on improving business practices. In the 19th century, the ESG started growing, and in 1898, the ‘Friends Fiduciary Corporation’ was established, connected with the Quaker movement and suggested investment strategies.

In the 1970s, Corporate Social Responsibility (CSR) increased momentum with the Interfaith Center on Corporate Responsibility, which was founded in 1971 and supports the business by advocating ethical practices.

During 20th-century events, in 1985, a hole was found in the ozone layer, and the Chornobyl disaster 1986 raised environmental awareness. In 1987, the Brundtland Commission’s “Our Common Future” report focused on sustainable development.

The first ESG Index Fund was introduced in 1990, and it integrated ESG criteria into business investment strategies.

The Carbon Disclosure Project was established in 2000 to improve corporate transparency regarding carbon emissions and climate risks. The ESG principles increased adoption in the 2010s, and in 2011, The Sustainability Accounting Standards Board (SASB) was established, which introduced industry-specific ESG reporting standards to improve the comparability and credibility of sustainability disclosures.

In India, before 2010, corporate social responsibility provided corporate accountability, but it didn’t have any structured reporting on environmental concerns. The Ministry of Corporate Affairs introduced the National Voluntary Guidelines for Environment and Business Responsibilities in 2011.

In 2012, the Security Exchange Board of India-SEBI asked companies to submit business responsibility and sustainability reports (BRSR), whereas in 2013, the Companies Act mandated companies to reinforce corporate responsibility. The Five Year Plan 2022-23 mandates companies for BRSR to increase transparency in business.

In this decade, there have been many agreements related to the ESG framework, the United Nations Sustainable Development Goals, the Paris Agreement in 2015 to address climate change concerns, and the Task Force on Climate-related Disclosures in 2015 to standardize financial reports related to climate change.

The Sustainable Finance Disclosure Regulation was launched in 2021, where ESG-related risks are disclosed. ESG integrates investment frameworks and corporate governance to increase transparency and accountability.

ESG Frameworks in India

India has made giant strides in ESG reporting, from voluntary CSR reporting to mandatory sustainability disclosures under the Securities and Exchange Board of India (SEBI). As seen earlier in 2012, SEBI made the Business Responsibility Report compulsory for the top 100 listed companies. In 2021, The Business Responsibility and Sustainability Report (BRSR) replaces BRR and extends obligations regarding ESG disclosures to the top 1,000 listed firms. Lastly, in 2023, SEBI will likely introduce third-party assurance for ESG reports to enhance transparency and reliability.

Strengths: BRSR of India has signed a lot concerning ESG, compared to many other structured disclosure law mandates.

Challenges: Limited enforcement, lack of standardization, and inadequate third-party auditing are obstacles to effective ESG reporting.

ESG Frameworks in the United States

The United States has been at the forefront of ESG reporting, with a well-established framework that has evolved over the years. The earliest ESG initiatives in the U.S. date back to the 1990s, highlighted by the introduction of the Ceres Principles (formerly known as the Valdez Principles) in 1989. Since then, various frameworks and guidelines have been developed, including:

Sustainability Accounting Standards Board (SASB): Provides industry-specific ESG reporting standards.

Global Reporting Initiative (GRI): Offers a comprehensive set of ESG reporting guidelines.

Task Force on Climate-related Financial Disclosures (TCFD): Focuses on climate-related risk reporting.

These frameworks have contributed significantly to the widespread adoption of ESG reporting in the U.S. Today, many U.S. companies, particularly those listed on the Dow Jones Sustainability Index (DJSI), publish annual ESG reports that provide stakeholders with valuable insights into their sustainability performance (Eccles et al., 2014).

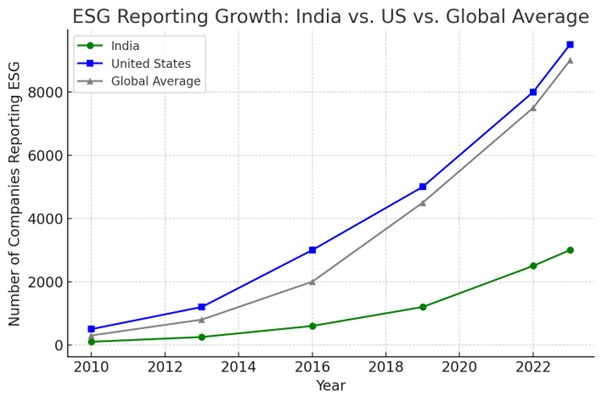

A Comparative Trend Analysis of ESG Reporting in India, US and World Average

The trend line graph below compares ESG reporting growth in India, the United States, and the global average from 2010 to 2023.

Key Insights:

ESG reporting in India has steadily improved, particularly from 2015, when SEBI set up BRSR (business responsibility and sustainability reporting).

While the USA has led in ESG reporting numbers, the growth is market-driven and not driven by regulatory factors.

Global ESG reporting mainly followed suit, revealing heightened investor demands and regulatory interventions around the globe.

The following are the visual graphs illustrating the trends regarding ESG reporting:

Global Growth in ESG Reporting (2010-2023)

This bar chart shows exponential growth in companies that report ESG metrics, especially after 2015, due to global mandates on sustainability and investor demand.

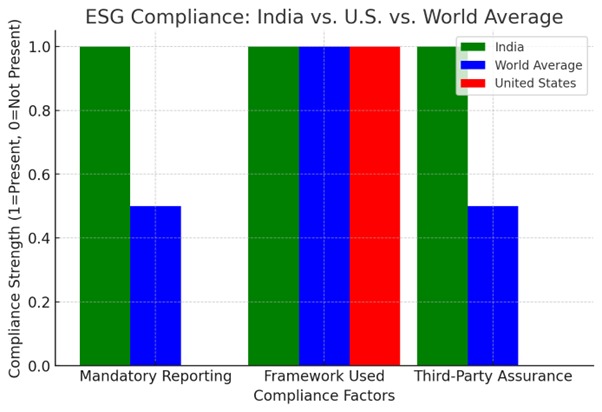

India Vs. US Vs. World Average concerning Compliance with ESG Norms

India is ahead in obligatory ESG reporting and third-party assurance, while the U.S. is critically behind in regulatory enforcement.

That average stands between India and the United States, signifying a slow but gradual global movement towards uneven adoption of ESG frameworks.

Significance and Impact of ESG Reporting

ESG reporting aims to create awareness of companies’ transparency and responsible conduct; there is doubt regarding its genuineness and efficacy. However, critics have argued that ESG reporting is merely symbolic and used as a marketing tool rather than a true expression of corporate conscience. That gets us to the interesting question: Is ESG just a show, or has it had a meaning in shaping global markets and policies?

Global Impact of ESG Reporting

Asset managers and institutional investors have begun integrating ESG factors into their decision-making processes. BlackRock, the world’s largest asset manager, has committed to investing in ESG. Governments and regulatory bodies have also responded by strengthening ESG disclosure requirements, particularly in the European Union (EU) and the United States (Amel-Zadeh & Serafeim, 2018). The ESG commitment forces many corporations to adopt new business models, namely net-zero commitments and social responsibility programs. However, the challenge that emerges is that companies exaggerate their ESG commitments, giving rise to greenwashing allegations. Lack of standardization among some ESG ratings has also been criticized for not accurately reflecting real-world impact.

ESG Reporting in India

India has considerably progressed toward ESG integration, with regulatory frameworks and investor demand acting as drivers. The Securities and Exchange Board of India (SEBI) has introduced the Business Responsibility and Sustainability Reporting (BRSR) framework, making ESG disclosures mandatory for the top 1,000 listed companies (SEBI, 2021). India was among the first nations to have mandatory CSR spending under the Companies Act of 2013, encouraging many corporations to adopt environmental and social initiatives. Nevertheless, these laws still leave out many Indian firms regarding standardized ESG reporting, making greenwashing a viable concern. There remains considerable inchoate knowledge of and compliance with ESG practices among small and medium enterprises or SMEs.

ESG Reporting in the United States

U.S. ESG reporting occupies a mixed landscape of regulatory oversight complemented by market-oriented initiatives. The Securities and Exchange Commission (SEC) has proposed new rules requiring climate-related disclosures to enhance transparency and comparability in ESG data (SEC, 2022). Large companies such as Apple, Microsoft, and Tesla are dedicated to ESG principles, especially in reducing carbon footprints and increasing workplace diversity.

Overall, ESG reporting has considerably influenced the framing of the corporate governance milieu and the investment construct globally. Nonetheless, the extent to which this has consequent real change is debatable. ESG reporting has thrust accountability and an element of transparency, but greenwashing and controversies about irregular regulations remain pertinent.

The Future of ESG Reporting

ESG reporting is evolving rapidly, fueled by regulatory needs, investor influence, and global sustainability goals. SEBI’s Business Responsibility and Sustainability Reporting (BRSR) for the top 1,000 listed companies mandatorily from FY 2022-23 brings ESG disclosure at par with global standards such as GRI and TCFD in India. CRISIL (2022) states that just 20% of Indian companies have a declared strategy to reach net zero, indicating the need for stricter regulation. The BRSR framework would be extended to SMEs and unlisted companies, further boosting sectoral transparency.

The United States has, through the SEC, proposed climate-related risk disclosure regulations, but it remains a politically charged issue regarding ESG disclosure. Despite regulatory challenges, 79% of U.S. large companies have made annual report ESG disclosures, paving the way for institutional investors BlackRock and Vanguard. The regulatory gap between needs and investor expectations means that voluntary ESG reporting will remain relevant.

Technological advancements are revolutionizing ESG reporting. Blockchain and artificial intelligence-based analytics are improving data quality and reducing the risk of greenwashing. EY (2021) stated that 54% of Indian companies have adopted third-party assurance for ESG data, reflecting a shift toward reliable disclosures. At the same time, governance and social factors are gaining significance. Indian public sector undertakings (PSUs) are more gender-balanced (15.3%) and less discriminative in wages than private companies, though private companies are further along in governance practices.

Capital allocation is becoming more closely associated with ESG performance in financial markets, recognizing sustainability as a primary driver of long-term economic strength. 69% of India’s top companies have set ESG-linked goals, prioritizing waste reduction, carbon management, and energy efficiency. Investors emphasize companies with good ESG scores, which has fueled growth in green bonds, sustainability-linked loans, and impact investments. Greater regulation, like SEBI’s mandatory BRSR, will drive transparency, and activist investors insist on better governance. ESG data will be more accurate due to technological advancements like AI and blockchain, ensuring accountability and avoiding the risk of greenwashing, further ensuring that ESG is a corporate imperative.

Conclusion

The evolution of ESG reporting from optional to mandatory disclosure as a regulation tool has occurred. India has a BRSR framework for higher regulatory enforcement while making the U.S. more reliant on voluntary initiatives for corporates to report on ESG initiatives.

The growing development of ESG reporting will impact the trend toward global standardization, regulatory enforcement, and assurance of data integrity.

References

Dun & Bradstreet. (n.d.). A Practical Guide to ESG

Interfaith Center on Corporate Responsibility. (n.d.). Our origin story

Cruz, C. A., & Matos, F. (2023). The ESG maturity: A software framework for the challenges of ESG data in investment. Sustainability, 15(3), 2610.

Amel-Zadeh, A., & Serafeim, G. (2018). Why and how investors use ESG information: Evidence from a global survey. Financial Analysts Journal, 74(3), 87-103.

Securities and Exchange Board of India (SEBI). (2021). Business Responsibility and Sustainability Reporting (BRSR) framework.

Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The Impact of Corporate Sustainability on Organizational Processes and Performance. Management Science, 60(11), 2835-2857.

Securities and Exchange Commission (SEC). (2022). Enhancing and standardizing climate-related disclosures for investors.

Gupta, R., & Motwani, A. (2022). ESG Reporting in India: Current Scenario. Corporate Governance Insight, 4(2), 88-104.

CRISIL (2022). CRISIL Sustainability Yearbook 2022.

KPMG (2022). Accelerating the Change: ESG Reporting 2.0.

EY (2021). The Evolving Non-Financial Reporting Landscape

One Response

Insightful!